When you invest in a specific stock, sector, theme (or meme), you’re basically saying you think it’s a better bet than all the other options out there. That is, any choice to invest in one thing is at the same time a choice not to invest in all other things. How sure can you be that such a narrow decision is the better one? Not at all (unless you’re breaking the law). Hard to fault the desire for excess return. But in theme-dominant market such as these, the shoulda-woulda-coulda thoughts that can drive one to chase stories can lead to poor choices:

- In the end, timing themes/trends/stocks is virtually impossible on a consistent basis. Resulting portfolio overweights can lead to disappointment when trends flag, fads stale, momentum shifts

- So, we seek broad diversification in an attempt participate…even if only partially…in any trend before it takes off. To the extent novel themes catch an unexpected bid, we may already own the names that might participate

- Will we generally “fully” participate in the latest market trends? Very likely not. But that works both ways: we might only partially participate in a trend after other investors have given it wings; but we also are very unlikely to unduly participate in trends adverse to the greater objective of success in achieving financial goals

What’s Your Angle?

Might be that the most important lesson an investor can learn is that, barring actions using the sorts of privileged information that constitute inside information, one can have no special insight into any stock’s, any sector’s or even the market’s near-, medium- or long-term future. No manner of “analysis” is going to result in your having more knowledge about tomorrow. So, all you have is an opinion. With that in mind, it is quite likely that your opinion is shared by some non-trivial portion of the investment universe. You and those folks have made that opinion known via your trades (or lack thereof…not having an opinion and not trading on an opinion is still a trade). Since those trades will have had some manner of impact on market prices, the market already reflects your opinion, along with the opinions of every other investor. When we say “reflects,” we mean to suggest that, so long as we require that the basis for owning any stock is the claim of future income from the issuer that ownership bestows on the owner of the stock, the current price represents the current value of all that future potential income (which need not be distributed to the investor, mind you; the income can be retained by the company for further investment). But that’s not all. Implicit in that price is the potential variability of the eventual outcomes versus what is presently expected, and not just in the context of that individual stock, but in the context of all securities (e.g., government bonds, corporate bonds, etc.). In easier terms, a stock’s price reflects every investor’s present assessment of the amount and likelihood of future income and capital gain relative to similar evaluations of every other stock (and potential other investments). These assessments will be different for each security across many axes, with relative value primarily relating to the price paid for expected growth and the expected variability of that growth across all stocks.

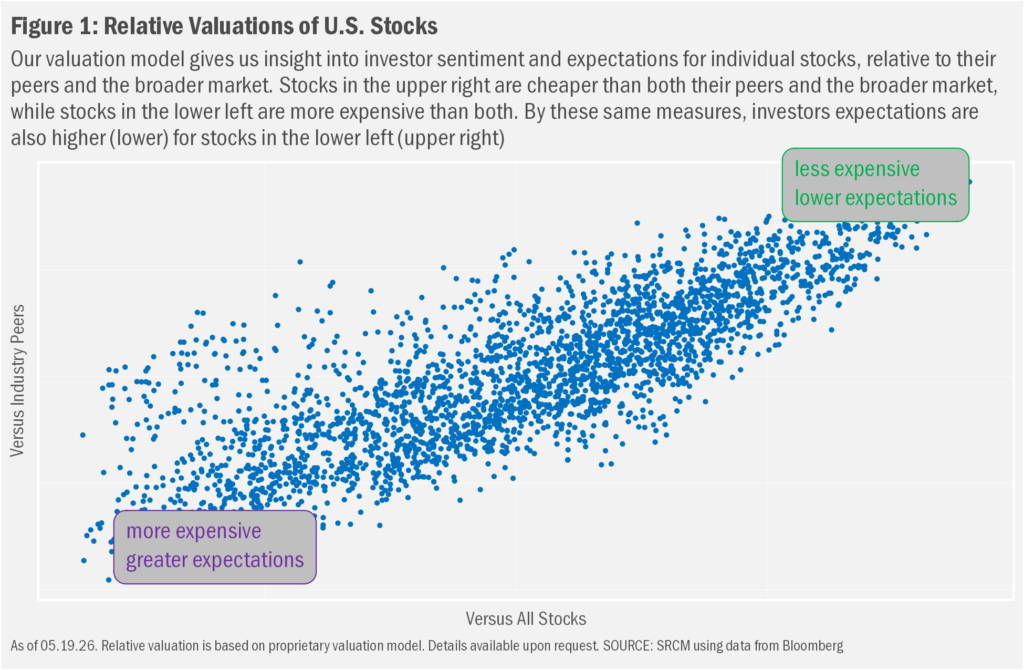

Why Relative Value Matters

We’ve homed in on relative value because that characteristic is core to how we should think about investing when it comes to our opinions regarding future developments. By relative value, we mean how attractive a stock’s current price is relative to its expected fundamentals and risk, compared with other investable alternatives. Stocks with low relative value reflect more aggressive expectations regarding future fundamentals. Dubbed “Growth” stocks for that reason, these stocks have captured investor interest in such a way as to raise their current prices relative to their current fundamentals to a level that “discounts” that future growth. In other words, Growth is already priced into these stocks and already incorporates consensus views regarding relative growth outcomes.

Of course, that investors believe the growth will come to pass does not mean that it will. More importantly, future returns depend not simply on whether growth occurs, but on whether the outcome is better or worse than what is already expected. Since prices of Growth stocks already reflect greater expected growth, those stocks are likely to underperform on a going-forward basis if expectations were too high. The historical tendency is such that actual growth can disappoint relative to what was priced in. So, we tend to think of Growth stocks as having low relative value. Naturally, the converse may be said of stocks with high relative value, for which investor expectations can be read as relatively low. These “Value” stocks reflect, variously, relatively weak investor confidence in the future relative improvement of their fundamentals.

Another way to look at Growth, versus Value, is that investors have assessed a lower risk that fundamentals will improve for Growth stocks, whereas they’ve adopted a “wait-and-see” approach for Value stocks. That is, they’re not called Growth stocks because they are better, they’re called Growth stocks because investors expect that they will be better. Might be that the “are better” has influenced the “will be better” bit, but it’s the latter that’ll matter most for future returns.

Importantly, theory suggests that investors aren’t making these assessments in a siloed manner. That is, one should believe that investors take all information and potential investment opportunities into consideration when making any decision. But we have the sense that theory is well removed from practice. The recent not altogether random, but at the same time mostly in our view irrational gyrations in individual stocks on account of memetic AI-related developments quickly come to mind. Even so, theory further suggests that, even if one or many individuals blindly consider one investment without regard to any other investment, other investors will trade in consideration of any resulting valuation mismatch (again, based on opinions regarding the future, which may or may not come to light).

Which brings us back to the opening of this commentary. When we understand that the current price of any market-traded security reflects all information—everyone’s observations and expectations for any individual investment, relative to all potential investments—we should be humble about assuming no one else shares our view. Otherwise, if you believe your opinion is that much different from everyone else’s, then you must also believe your expected outcome is relatively unlikely. If it were more likely, more people would share that view and the market price would more closely reflect it. In that context, you must also believe your opinion points to additional gain beyond what is already priced in. More importantly, it must also lead you to want to overweight that perceived opportunity relative to all the other opportunities you might consider.

So, for any specific bet on the future to be “correct”, it must be sufficiently distinct from what’s already priced in, while also being optimal relative to all other potential uses of capital. We find all those hurdles far too high to clear on a regular basis.

Stocks Gonna Stock

Since markets already reflect the consensus view of future fundamentals and risk, outperformance requires being right where the market is wrong—and right enough to justify the portfolio tradeoff. That is why we generally believe investors are better off letting stocks do what stocks will do. Prices will rise and fall based on factors we cannot control. So, we prefer to own at least some portion of many, many stocks, allowing us to possibly participate in future developments that are not yet priced in. That does not mean we believe investors should always take a purely passive approach, though that can be entirely appropriate. As noted in the Growth-versus-Value discussion above, we favor an approach that recognizes how differences in investor opinion can cause stocks to exhibit characteristics associated with higher expected returns. Because it can take time for those expected returns to emerge, we generally tilt portfolios toward those characteristics in a systematic, diversified way. This allows us to pursue expected return differences without relying on concentrated predictions. In our view, that design preserves more market-like return behavior while still giving the portfolio a chance to benefit from what we believe are more thoughtful equity allocations.

As we have learned first-hand over the many years we have been investing portfolios, this approach requires massive and expensive datasets, extensive analytics, thoughtful portfolio design and careful implementation. And in order to achieve the additional expected return an overweight to these observably more attractive characteristics presents, the approach must remain lean from a cost perspective. Hence, our preference for a fund-based methodology. Most importantly, the funds now available to us provide exactly the manners of investment we might otherwise directly implement ourselves. Further, the fund-based approach in practice allows for much broader (i.e., more individual stock holdings expressing favored characteristics) and much more adaptable portfolio implementation, potentially providing greater diversification, lower turnover costs, operational efficiency and tax-management advantages depending on vehicle/account type. By most metrics, then, the funds-based approach is the better one from both the mechanics and efficiency perspectives. By the way, we implement a necessarily different but methodologically consistent approach within fixed income.

More May Not Be Better

The modern finance industry is never short of shiny new things to sell. Most rely on some manner of belief that the simpler approach is suboptimal, perhaps even wrong. Even without the help of industrial finance , investors can find themselves constantly drawn to new opportunities and regularly tempted by the possibility of excess gain relative to how their portfolios are currently positioned. We admit that the instinct to seek greater gain is natural, if only because it seems possible. But that instinct can be checked with a combination of intuition and math. When we review most of these pitches and do the work required before implementation, we usually find that the shiny option compares poorly with the tried and true across the most probable range of outcomes. In the end, we have learned through such work and direct experience that there generally are rather few reasons to layer additional complexity on a portfolio over our present method (even as that method has evolved over time) in the pursuit of a more optimal path to reach client financial goals. More often than not, we end up circling back to our existing strategies. That does not mean that our approach never changes. And even within our approach, there’s a fluidity intentionally embedded in the style that’s meant to adapt to changing opportunities. Ultimately, the work that tends to curb most adventures is the same that led us to the financial planning and investment methodologies we implement today.

Most importantly, we have learned that clients have historically found greater comfort in understanding that, while there is little we can know about the future, there is much we can learn from the past. If we accept a reasonably identifiable level of uncertainty, we may find that the reward over time has been sufficient compensation for bearing it. In the meantime, we should seek to balance comfort with investment risk and the desire for investment reward in the most efficient, understandable, and practical way available.

Important Information

Signature Resources Capital Management, LLC (SRCM) is a Registered Investment Advisor. Registration of an investment adviser does not imply any specific level of skill or training. The information contained herein has been prepared solely for informational purposes. It is not intended as and should not be used to provide investment advice and is not an offer to buy or sell any security or to participate in any trading strategy. Any decision to utilize the services described herein should be made after reviewing such definitive investment management agreement and SRCM’s Form ADV Part 2A and 2Bs and conducting such due diligence as the client deems necessary and consulting the client’s own legal, accounting and tax advisors in order to make an independent determination of the suitability and consequences of SRCM services. Any portfolio with SRCM involves significant risk, including a complete loss of capital. The applicable definitive investment management agreement and Form ADV Part 2 contains a more thorough discussion of risk and conflict, which should be carefully reviewed prior to making any investment decision. All data presented herein is unaudited, subject to revision by SRCM, and is provided solely as a guide to current expectations.

Past performance is not a guarantee or reliable indicator of future results. The opinions expressed herein are those of SRCM as of the date of writing and are subject to change. The material is based on SRCM proprietary research and analysis of global markets and investing. The information and/or analysis contained in this material have been compiled, or arrived at, from sources believed to be reliable; however, SRCM does not make any representation as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated thereby. Any market exposures referenced may or may not be represented in portfolios of clients of SRCM or its affiliates, and do not represent all securities purchased, sold or recommended for client accounts. The reader should not assume that any investments in market exposures identified or described were or will be profitable. The information in this material may contain projections or other forward-looking statements regarding future events, targets or expectations, and are current as of the date indicated. There is no assurance that such events or targets will be achieved. Thus, potential outcomes may be significantly different. This material is not intended as and should not be used to provide investment advice and is not an offer to sell a security or a solicitation or an offer, or a recommendation, to buy a security. Investors should consult with an advisor to determine the appropriate investment vehicle.