Wall Street loves itself a forecast. Fulfilling that want, there are groups of folks whose business it is to estimate the future paths of most meaningful financial metrics. Regular readers know we don’t place too much stock, as it were, on market or macroeconomic prognostications. As generally unreliable as they might be, though, we don’t find those data altogether uninteresting:

- Much as math might be involved in these efforts, all estimates are qualitatively driven at their core. Like most such behavioral measures, then, they may be indicative in the aggregate of investor sentiment, which may help explain market movements in the nearer term

- Revisions to such estimates over time reflect an important tenet of financial planning. Since financial plans also generally are chock-full of estimates, the planning process should include regular reviews of and updates to those estimates. Not only do those reviews allow for an honest assessment of any plan’s viability, such reviews enable regular adaptions to help ensure the plan remains on path toward goals

Coming Back ‘Round

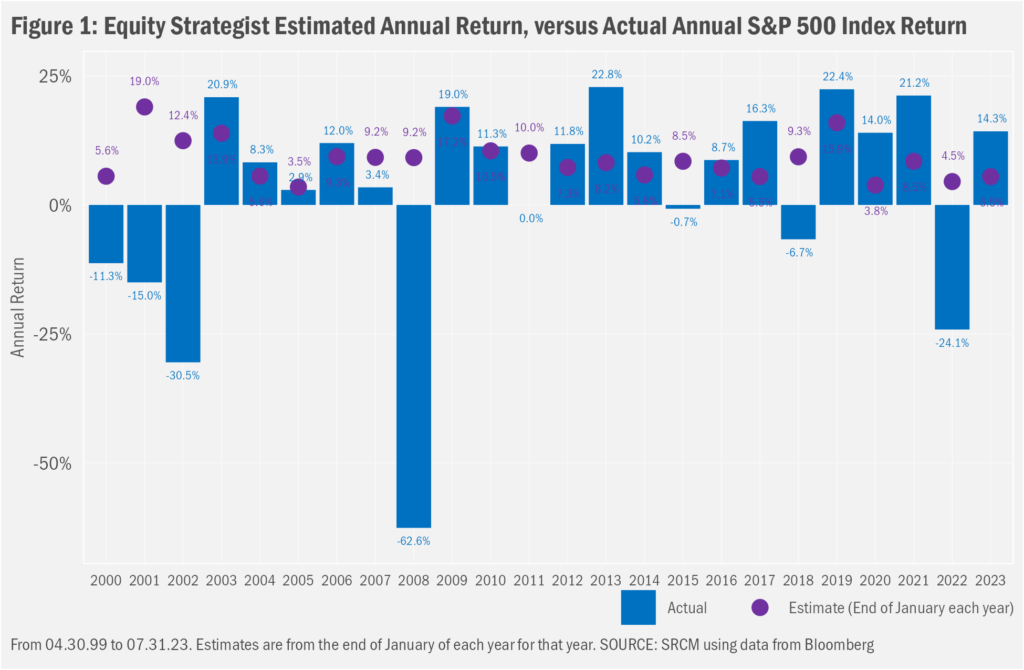

U.S. stock strategists are challenged to predict the year-end value of the S&P 500 Index. We have to think that work is among the more pointless endeavors in finance. Providing a point estimate a year out is pure guesswork, while the closer we get to the end of the year, the more matter-of-fact the target becomes. Further, a cursory review of past data suggests that estimates near the beginning of the year tend to be in the high single digits, except when the prior year was more-than-normally good or bad, in which case the estimates tend to be either lower or higher than tendency. The upshot is that those early estimates, at least in the aggregate, amount to a reflection of equity market norms, which are that annual stock market returns tend to be positively biased and average in the high single digits (the simple annual average return of the S&P was 9.3% in the 25 years ended 2022 and 12.0% since 1926). So, guessing somewhere in the 8-10% range seems rational, and just about likely to prove on-target, unless it doesn’t, in which case, “Oh, well!”

Coming to Term

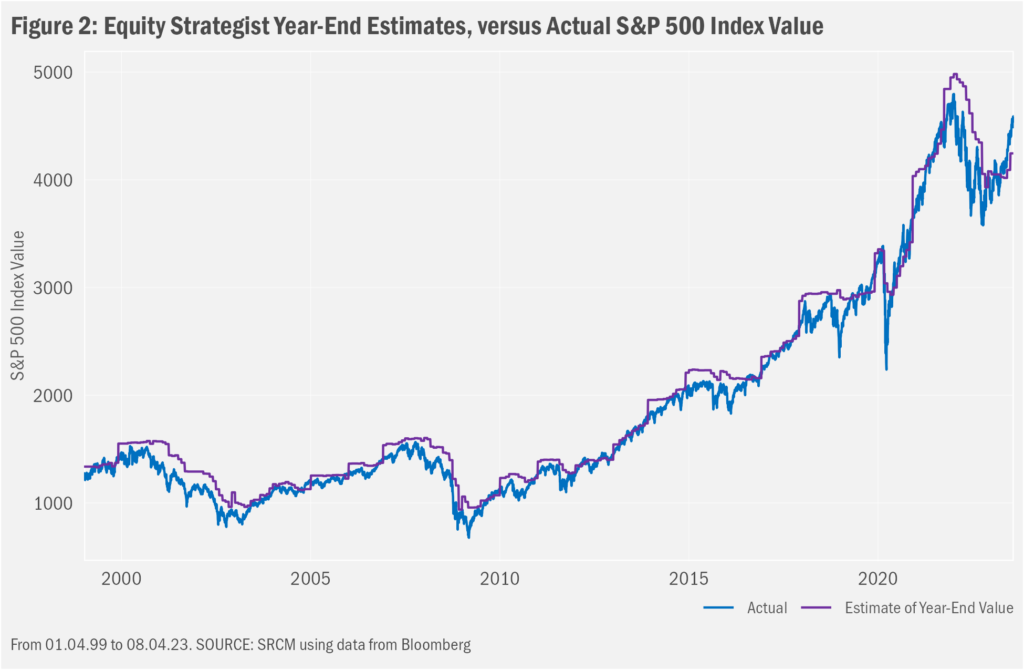

Reviewing data over shorter time frames, more interesting tendencies come to light. Looking at Figure 2 (we say “looking”, as this is a 100% visual analysis, not a statistical one), we find a tendency for estimates to mirror the aggressiveness in markets with strong upward momentum (the purple estimate line tracks the upward path of the actual index value). In less ebullient markets, we see an inclination to retain a generally positive outlook (the estimate line hangs above the actual line). This gap tends to be larger in down markets, when estimates seem to expect an eventual rebound, until a strong-enough bounce arrives, and estimates begin to track the ongoing gains.

In that context, it’s worth highlighting present estimates, which in the aggregate still call for material downside through year end (the end-of-July estimate was for a year-end value of 4245, versus the latest S&P closing value of 4478). Even as estimates have risen along with this year’s gains, there must still be a good bit of, “well, we’ll be right eventually” driving still relatively pessimistic expectations.

And you know what? That stance may well be warranted, if not in terms of timing or of the specific level to be reached during the drawdown, but in the notion that drawdowns are fundamental to the investing experience. That’s not meant as a warning, as it’s always helpful to remember that markets are naturally volatile. And that longer-term gains are better thought of as just reward for the patience required to endure market drops. When inevitable downturns arrive, it helps to remember that, until this latest bout, markets have always rebounded from drawdowns. And even as markets are amidst a rebound and in particular when they are reaching for fresh highs (again, not there yet, but we’re well on our way…), it helps to maintain the understanding that declines are possible, almost certain over short- and medium-term timeframes. Reflected in the work of Wall Street strategists, a rational mix of optimism in the face of market tumult and caution against bountiful gains are part of what we have found to be pragmatic perspective when planning for financial goals.

Important Information

The opinions expressed herein are those of SRCM as of the date of writing and are subject to change. The material is based on SRCM proprietary research and analysis of global markets and investing. The information and/or analysis contained in this material have been compiled, or arrived at, from sources believed to be reliable; however, SRCM does not make any representation as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated thereby. Any market exposures referenced may or may not be represented in portfolios of clients of SRCM or its affiliates, and do not represent all securities purchased, sold or recommended for client accounts. The reader should not assume that any investments in market exposures identified or described were or will be profitable. The information in this material may contain projections or other forward-looking statements regarding future events, targets or expectations, and are current as of the date indicated. There is no assurance that such events or targets will be achieved. Thus, potential outcomes may be significantly different. This material is not intended as and should not be used to provide investment advice and is not an offer to sell a security or a solicitation or an offer, or a recommendation, to buy a security. Investors should consult with an advisor to determine the appropriate investment vehicle.