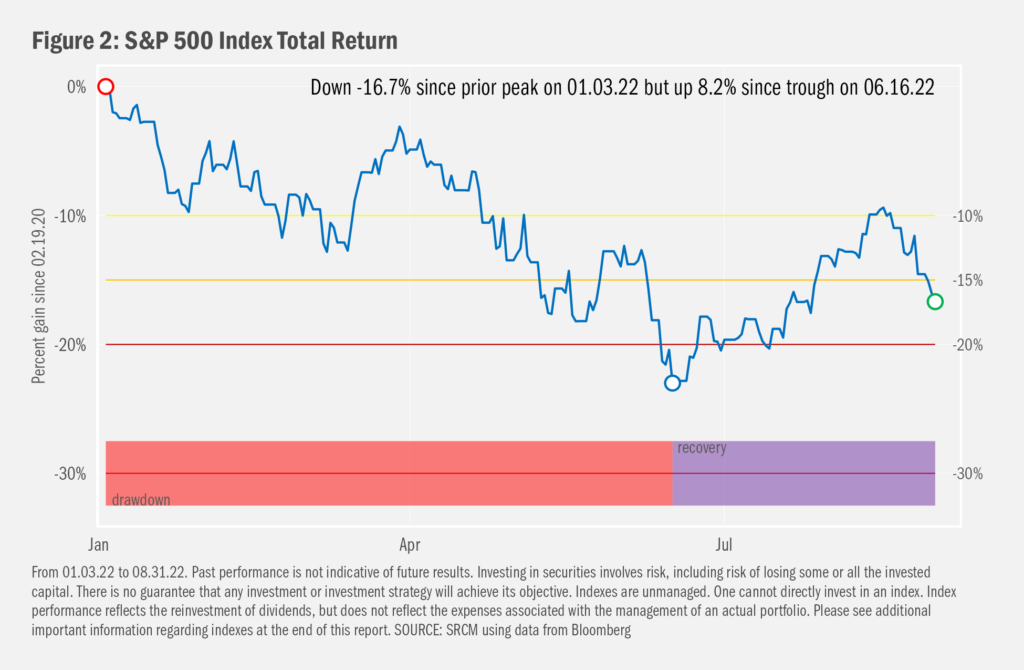

We were having such a good time, weren’t we? After dropping more than 20% from the beginning of the year through mid-June, the market staged a convincing rebound as investors seemingly saw fit to look beyond the complexities of central bank policy, maybe trusting that inflationary forces could be weakened and might otherwise work themselves out over time. That rebound has stalled, but one shouldn’t be surprised. Investors need not forget:

- With sources of rising and otherwise still-high prices so diverse, there’re no quick fixes to present challenges

- Impatience is understandable as trends remain indecisive. Even so, we’ve begun to see favorable shifts in the data, which lend credibility to the current courses of action

- But there’s always a tomorrow. Facts can change such that more or less effort and/or time may be required for inflation to return to tamer levels, and employment and growth may suffer as a result

- Meantime, stock and bond markets likely will remain volatile as investors take varying cues from fresh data as they arrive

Listen to this month's Notes from the CIO Podcast:

Podcast: Play in new window

Subscribe: Apple Podcasts | RSS

A Bit about Inflation…

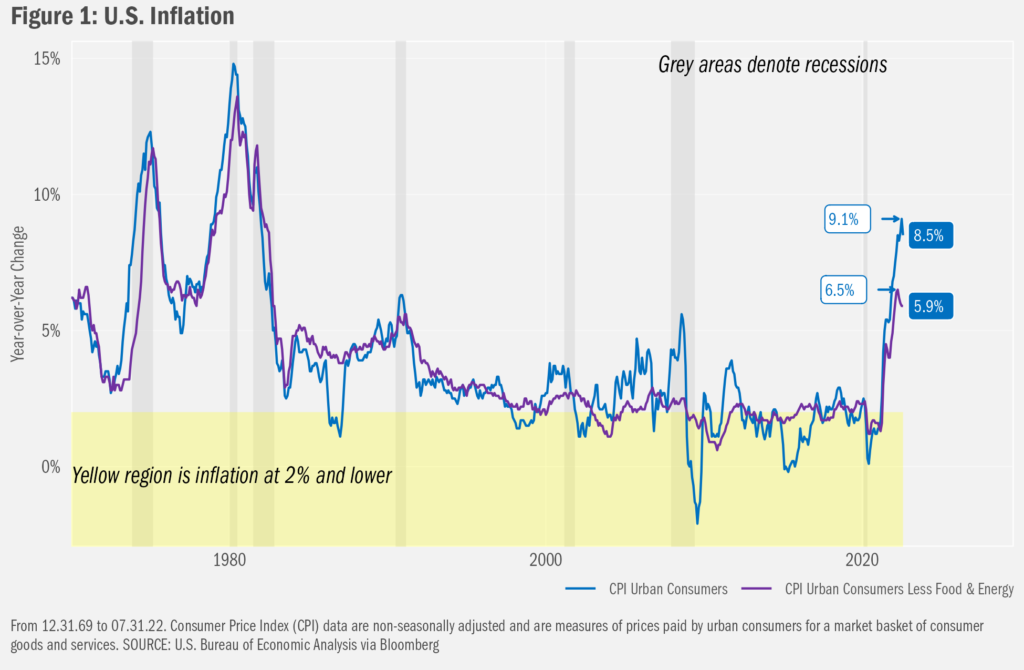

Putting the current rate of inflation in context, we see that the U.S. consumer has not seen a rate of change in prices this high since the 1980s. The surge comes after more than a decade of reasonably calm inflation, the rates of which rolled around the collectively desirable 2% range, a level set for its not-too-cold/not-too-hot tendency to give folks little reason to pay attention to it. But a collection of forces applied upward pressure on prices after the initial global COVID shutdown. First, that shutdown brought global supply chains to a near standstill. From raw materials to finished goods, product deliveries stalled and often halted, leaving final supply low relative to demand. Since scenarios in which levels of demand exceed supply tend to see prices pulled higher, inflation began to rise. Well before those supply chain challenges began to ease, though, governments around the world provided vast fiscal and monetary stimuli to jolt their economies back to life. These funds tended to enhance demand—in many segments beyond what otherwise might have been desired without the excess funds—further expanding the mismatch between supply and demand. Next came the war in Ukraine, which wreaked further havoc on supply chains just as they were beginning to gain post COVID-crisis momentum. Particularly hard hit were grains and other foodstuffs sourced from Ukraine (again, lower supplies for a given level of demand). Energy supplies—for Europe most starkly—were crimped by a combination of sanctions-related import restrictions on Russian oil and gas, and Russia’s restrictive responses to those actions. Various other mostly raw material (e.g., raw and processed metals) and some finished goods (e.g., a range of automotive goods) saw shipments slow or cease as Ukrainians focused attention on the war.

The Levels, They Are A-Changin’

What’s important to remember about inflation, though, is that it is a measure of the change in prices, not the level of prices. That is, prices may remain high in historical context even as inflation drops. The American Automobile Association shows the average price of a gallon of regular unleaded gasoline in the U.S. at $3.841 on August 31. It could linger at this relatively high level (the average of daily values since August 1992 is $2.827), perhaps by trending more sluggishly downward. Markets nonetheless might continue to think positively even of a slower inflation unwind, despite ongoing consumer distress over the still-high cost to fill the tank.

Good news, then, that gasoline prices in fact have actually fallen pretty dramatically since peaking at $5.016 on

June 13 of this year. Same for global food prices: bulk costs for corn, rice, palm oil and wheat are at or below pre-war levels. Both groups of prices (energy and food) tend to be volatile, which is why folks tend to focus on inflation excluding those two groups (Figure 1 shows inflation with and without energy and food). But inflation outside of energy and food have been easing as well (latest readings show a decline in both series). Which brings us to a more critical point with regard to how markets seem to respond to these sorts of data. While levels are important—the rate of inflation remains historically high—the hooks at the end of both lines are what matter more to investors now. That is, the fact that the rate of inflation is slowing means we may be on the path back to more favorable price stability.

Eyes Forward

Much as we noted in last month’s commentary discussing recessions, markets will tend to react to incrementally positive shifts in economic trends to get in front of a return to macroeconomic expansion (and vice-versa, of course). It has not been surprising, then, to have seen the stock market respond positively to initial signs that inflation might be slowing, while the broader economy seemed not yet to feel a burning sting from the bite of higher interest rates. That’s the bounce from the June lows. Even so, we must note that the sting isn’t abating, and may we worsening. For example, higher mortgage rates seem to have crushed home sales. There, both levels are low and the rate of change has been increasingly negative. Waning housing demand is among the incremental changes of the worrisome sorts, of which there are a few. Hence the stall in the market rebound.

Those two states of affairs—easing energy and food prices amidst plunging home sales—reflect the balance that must be struck such that we might march an orderly path out of the presently distressing state of affairs. Top of mind for investors seems to be whether the Federal Reserve, which sets the tone for interest rates across the economy as part of its mandate to maintain stable prices and full employment—and thereby demand for credit, which can be used to fund additional purchases, investment and growth—will be able to support the cooling of inflation without placing too heavy of a hand on employment or growth. Since the Federal Reserve arguably can have little impact on global supply chains outside of, as an example, the potentially negative impact on incremental investment in supply that might stem from higher interest rates, much attention is focused now on what’s historically seen as among the more permanent drivers of inflation: workers’ wages. As prices remain high, with little sense of an easing in inflation, while the unemployment rate remains historically low, workers may begin to require greater pay for the same amount of work (demand for labor stays the same or as is generally the case grows, while the supply of labor for a given price level falls). Wage inflation tends to be stickier, as workers are unlikely to settle for less once more has been achieved. And those extra dollars might actually worsen inflation (more demand for a given level of supply) such that prices might continue to rise, spurring additional wage increases, and so on in a ruinous cycle.

Thankfully, we’re not there yet: wage growth remains high, but the rate of increase also has been slowing over the past several months. But one cannot rule out a disastrous wage-price spiral just yet. Happily, a range of measures express expectations for inflation to slow. But expectations are not reality, so one neither can yet confirm a not-too-harsh impact on growth and employment from higher interest rates potentially set in order to tame inflation that persists longer than presently expected. Investors therefore are apt to focus on each new metric that reflects shifts in supply, demand, the prices at which the factors two meet and the resulting net change in aggregate employment and growth. Those details are likely to remain volatile in pace and direction, while often spawning mixed views as investors differently weigh each datum and alter prognoses. Stock and bond markets will reflect that changing of attitudes and positioning, likely a source of ongoing volatility. Even so, just as was the case at the depths of COVID-crisis uncertainty, we continue to believe that the optimal approach for most investors is to adhere to an existing investment plan established prior to this latest drawdown, so long as financial situations and constraints do not differently require. And we again will remind folks that it’s often during times such as these that a conversation with an advisor may support the historically more favorable stay-the-course stance when thoughts might lead actions otherwise.

Important Information

Signature Resources Capital Management, LLC (SRCM) is a Registered Investment Advisor. Registration of an investment adviser does not imply any specific level of skill or training. The information contained herein has been prepared solely for informational purposes. It is not intended as and should not be used to provide investment advice and is not an offer to buy or sell any security or to participate in any trading strategy. Any decision to utilize the services described herein should be made after reviewing such definitive investment management agreement and SRCM’s Form ADV Part 2A and 2Bs and conducting such due diligence as the client deems necessary and consulting the client’s own legal, accounting and tax advisors in order to make an independent determination of the suitability and consequences of SRCM services. Any portfolio with SRCM involves significant risk, including a complete loss of capital. The applicable definitive investment management agreement and Form ADV Part 2 contains a more thorough discussion of risk and conflict, which should be carefully reviewed prior to making any investment decision. All data presented herein is unaudited, subject to revision by SRCM, and is provided solely as a guide to current expectations.

The opinions expressed herein are those of SRCM as of the date of writing and are subject to change. The material is based on SRCM proprietary research and analysis of global markets and investing. The information and/or analysis contained in this material have been compiled, or arrived at, from sources believed to be reliable; however, SRCM does not make any representation as to their accuracy or completeness and does not accept liability for any loss arising from the use hereof. Some internally generated information may be considered theoretical in nature and is subject to inherent limitations associated thereby. Any market exposures referenced may or may not be represented in portfolios of clients of SRCM or its affiliates, and do not represent all securities purchased, sold or recommended for client accounts. The reader should not assume that any investments in market exposures identified or described were or will be profitable. The information in this material may contain projections or other forward-looking statements regarding future events, targets or expectations, and are current as of the date indicated. There is no assurance that such events or targets will be achieved. Thus, potential outcomes may be significantly different. This material is not intended as and should not be used to provide investment advice and is not an offer to sell a security or a solicitation or an offer, or a recommendation, to buy a security. Investors should consult with an advisor to determine the appropriate investment vehicle.

The S&P 500 Index measures the performance of the large-cap segment of the U.S. equity market.

One cannot invest directly in an index. Index performance does not reflect the expenses associated with the management of an actual portfolio. Investing in any investment vehicle carries risk, including the possible loss of principal, and there can be no assurance that any investment strategy will provide positive performance over a period of time. The asset classes and/or investment strategies described in this publication may not be suitable for all investors. Investment decisions should be made based on the investor's specific financial needs and objectives, goals, time horizon, tax liability and risk tolerance.